Image

Regional integration in Africa is underway but progress requires that the gains are widely spread. South Africa’s huge regional trade surplus in manufactured goods is leading to protectionist pressures in neighbouring countries. Agro-processing is a large sector that has significant potential, but the export performance of the region has been poor if South Africa is excluded. Regional value chains are failing to include the small economies of southern Africa. Constraints include tariff and non-tariff barriers, weak infrastructure, as well as poorly developed local suppliers. Some retail chains, supported by governments and NGOs, are now taking the lead in developing small-scale suppliers in the region. But other policies to improve the regulatory and investment environment are also necessary.

There is a clamour of excitement around regional integration in Africa. The recently ratified African Continental Free Trade Area (AfCFTA) is an important step towards the long-term goal of regional integration and a big boost to regional trade and industrialisation. Regional integration will be driven in part by growing trade links, and it is expected to facilitate the development of regional value chains. However, ongoing progress will require active policy measures to promote the spread of benefits to all the countries involved. In southern Africa, South Africa’s dominance and huge regional trade surplus in manufactured goods are already an issue.

Most southern African countries’ exports remain highly resource- and agriculture-dependent (African Economic Outlook 2019). Much of this trade is destined for markets outside of Africa, with intra-regional trade flows generally low. Yet the opportunity for expanding agro-processing exports within the region through the AfCFTA is significant (Fukase and Martin 2018). Agro-processing links to agriculture make it potentially pro-poor. It is also a sector where certain southern African countries have demonstrated comparative advantage in particular products.

This article, based on a UNU-WIDER paper, reviews the case for agro-processing both from a growth and development perspective. We look at agricultural and agro-processing trade in the region, including participation by countries in regional and global value chains, and examine the constraints. We focus particularly on how South African food processors and supermarket chains can upgrade regional value chains and develop small suppliers. We go on to consider what policies could best accelerate the process of regional integration.

The potential of the agro-processing sector is far from being realized. Export performance in many countries has been poor and South Africa has a large ongoing trade surplus with the region. While regional value chains in food production and distribution have developed, they are failing to include the small economies of southern Africa. Participation is constrained by a weak investment climate, barriers to trade, and the lack of domestic supply capacity. This problem needs to be addressed by improving the investment climate but also by measures to assist the development of suppliers in South Africa’s neighbouring countries.

In general, African economies are characterized by low levels of industrialisation. Manufacturing accounts for a low and declining share of value added, and manufacturing exports lag those of the rest of the world.1 While participation in international trade in manufactured goods has increased, this primarily involves low value-added, resource-based products (African Economic Outlook 2019). This is slightly less true for intra-African trade, which has a higher proportion of value-added products, but intra-African trade remains low relative to that of other regional trade blocs.

With its goal of easing trade restrictions between African countries and simplifying the complex groupings of regional trade agreements that currently raise costs of trade in Africa (African Trade Report 2018), the adoption of the AfCFTA could be an important instrument to boost intra-African trade and industrialisation.

Some are sceptical, however, arguing that southern Africa represents a protected market for South African goods and that South Africa is unlikely to support the relocation of production activities to neighbouring countries (Scholvin 2018). While South Africa’s economic size provides a large potential market for the countries of the region, there is currently a significant trade imbalance, with South Africa dominating the supply of processed and manufactured products (Banga and Balchin 2019).

Agriculture has always been essential to development. Recently, however, there is a renewed focus on the sector as a central driver of development in lower income countries, rather than simply playing a supporting role for manufacturing and industrial production (Fukase and Martin 2018). The ‘premature’ deindustrialisation being faced by many African countries and the shrinking space in a manufacturing industry dominated by low-wage production in economies like Bangladesh and Vietnam, have meant that southern Africa must seek to achieve growth in new and innovative ways (Mazungunye 2019). Value-added trade in agriculture and agro-processing may be one such opportunity, especially given its strong impacts in rural areas and the major role for women and seasonal workers. Fukase and Martin (2018) argue that regional agricultural trade, and specifically trade in agro-processed goods, could facilitate industrialisation if governments are able to lower tariffs, increase trade facilitation, and reduce transport costs.

In addition to agro-processing offering a promising path to development, Geyer (2019) argues a regional focus is likely to be the most beneficial for southern African countries. He demonstrates that these countries tend not to benefit from participation in Global Value Chains (GVCs) because of the low value added in products exported. In contrast, the value added of products exported within the region is higher, suggesting scope to enhance the gains from trade through the development of industries linked through Regional Value Chains (RVCs). But South Africa’s regional dominance is key to understanding the structure of RVCs, thus creating greater balance between it and the rest of the region is important for better regional integration (Odijie 2018).

The links to agriculture, including smallholder agriculture, also make growth in agro-processing potentially pro-poor (African Economic Outlook 2019). Agro-processing has the potential to provide a bridge from primary agricultural products to industrialisation, while boosting demand for agricultural products and increasing opportunities for rural employment (Mazungunye 2019, Owoo and Lambon-Quayefio 2018). This is illustrated by Tanzania, where growth in agro-processing reduced reliance on a relatively small basket of products, mostly primary resources and raw agricultural goods. In addition, it increased the employment of women in rural areas, and, through strong forward and backward linkages in the economy, provided a bridge to growing industrial sectors such as farm equipment, retail, and transport industries (Mazungunye 2019).

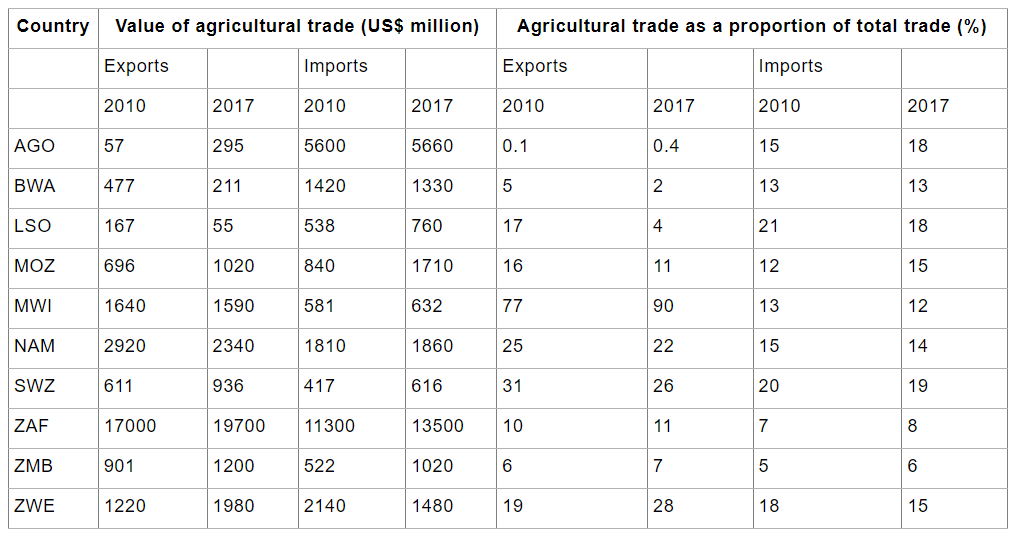

Table 1 shows the significance of agricultural (raw and processed product) trade to each country in the region, reflecting the values (US$ million) of trade in agricultural products as well as its share in the country’s total trade from 2010 to 2017. This varies significantly across countries. South Africa dominates by a substantial margin both exports and imports in terms of value. All countries, apart from Angola, Botswana, Lesotho, and Mozambique, were net exporters of agricultural products in 2017.

Table 1: Agricultural trade between southern African countries and the world

Notes: Mirror data (i.e. data reported by the trading partner) used for Eswatini in 2010. The three-digit country classifications in parentheses for each country are Angola (AGO), Botswana (BWA), Eswatini (SWZ), Lesotho (LSO), Malawi (MWI), Mozambique (MOZ), Namibia (NAM), South Africa (ZAF), Zambia (ZMB), and Zimbabwe (ZWE).

Source: Authors’ calculations based on UN Comtrade data.

Table 1 also reflects the different levels of growth in agricultural trade for each of these countries. Six countries have grown the value of their agricultural exports, with over 50% growth experienced by Angola (off a low base), Eswatini, and Zimbabwe. Four countries have seen declining agricultural exports, by more than 50% in the case of Botswana and Lesotho. Interestingly, the change in the share of agricultural exports does not always track the changes in their value —agricultural products make up a higher proportion of Malawi’s exports, despite decreasing in value, while Eswatini’s agricultural industry has grown in value, but has lost ground in its share of exports.2

For several countries, there is substantial volatility in export values and shares between 2010-2017. There is also significant heterogeneity in agricultural trade across these countries, both in terms of absolute growth of the industry and in how the industry has grown relative to the overall trade economy. Only six of the eight countries experienced positive export growth. Importantly, imports of agricultural goods constitute a relatively high proportion of overall imports signifying the potential to increase intra-regional trade.

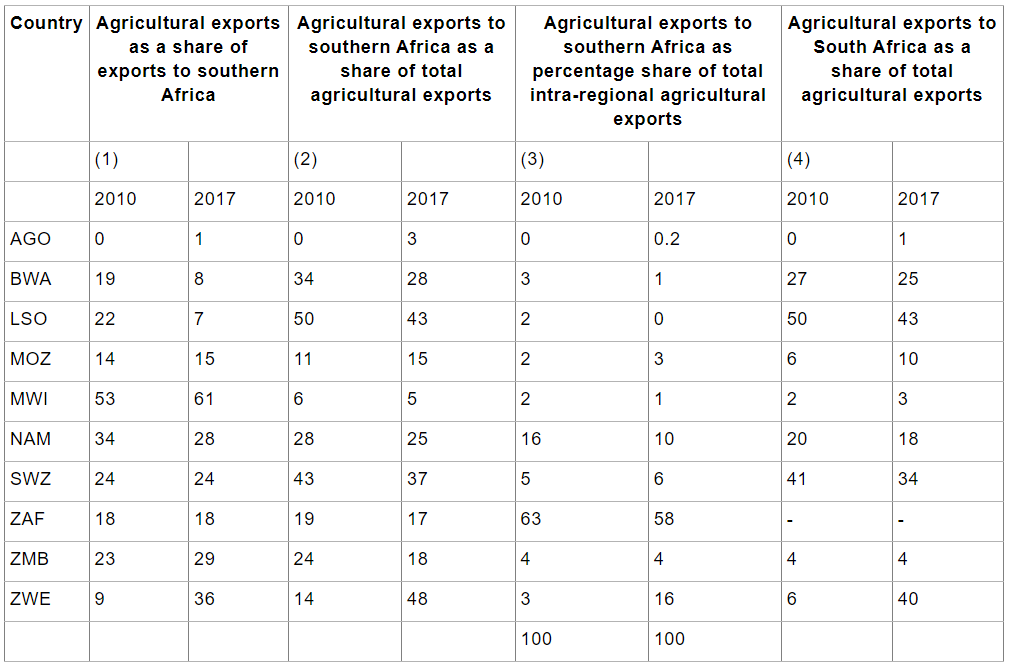

Table 2 shows several indicators of intra-regional trade in agricultural products.

Table 2: Intra-regional agricultural trade in southern Africa (%)

Notes: Mirror data used for Eswatini in 2010.

Source: Authors’ calculations based on UN Comtrade data.

The first two columns indicate the important role that the region plays for many of these countries’ agricultural industries. Apart from Malawi and Eswatini, agricultural exports comprised a higher share of exports to the region compared with exports to the rest of the world in 2017. There is also a relatively high share of total agricultural exports destined for the region (as shown in column 2). Agricultural trade is therefore regionalized.

But there are no clear patterns emerging. Intra-regional agricultural exports have not grown as significantly as might be expected given these countries participation in the Southern African Development Community (SADC) free trade area that began in 2000. Column (4) also reveals that the bulk of agricultural exports to the region are destined for South Africa. Agricultural exports to the rest of the region are limited.

The third column further demonstrates the unbalanced nature of agricultural trade within the region. South Africa’s share of intra-regional agricultural exports was almost two thirds in 2010, although this declined to 58% in 2017. While South Africa is an important market for most of these countries’ agricultural exports, the country still runs a significant trade surplus with the rest of the continent. In 2018, South Africa’s agricultural exports to the region amounted to US$3.3 billion compared with imports of US$1.09 billion. The unbalanced nature of trade is also reflected in the fact that South Africa sources only 8.1% of its total agricultural imports from the region.

The role of agro-processing

The above analysis has focused on all agricultural products, raw and processed. This section focuses on the relative importance of agro-processing trade, as it is this that gives rise to the potential to develop RVCs.

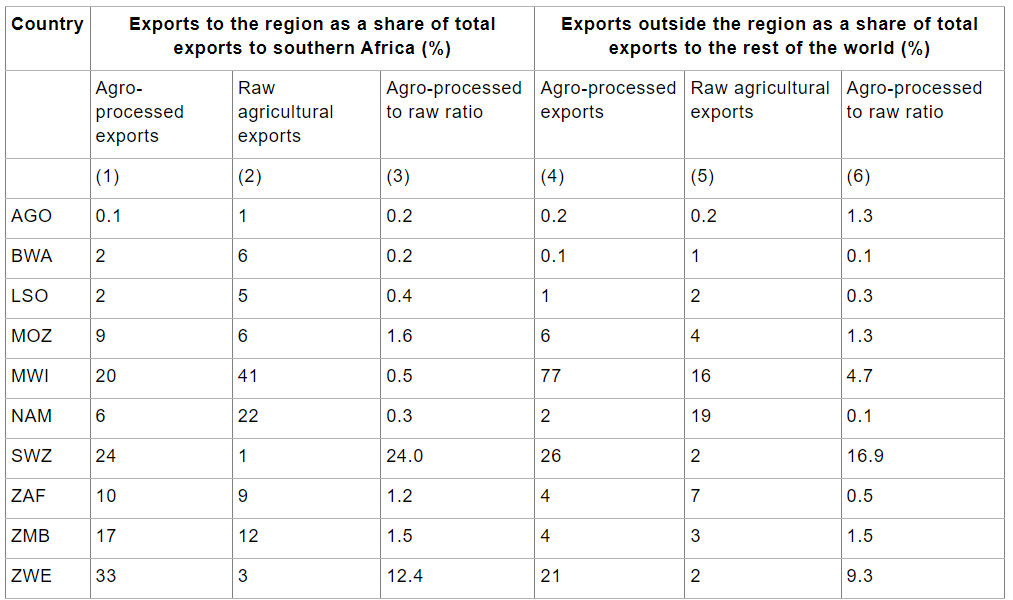

Table 3 presents data on the exports of raw and processed agricultural products to the region and to the rest of the world for 2017. Several features are evident here.

Table 3: Relative importance of types of agricultural products to intra- and extra-regional trade in 2017

Source: Authors’ calculations based on UN Comtrade data.

Firstly, a high proportion of agricultural trade comprises agro-processed goods. For half the countries in the sample, the value of processed agricultural exports to the region exceeds the value of raw agricultural exports. The gap is particularly large for Eswatini.

Second, for most countries, agro-processing plays a more important role in exports to the region than it does in trade with the rest of the world. On average, agro-processing’s share of total exports to the region is higher than its share of exports outside of the region. The exceptions are Angola, which has a very small agricultural industry, and Malawi, which has a very dominant tobacco industry.

Performance in agricultural exports has been mixed with several countries experiencing a decline. Intra-regional trade tends to be more agricultural intensive than exports to the rest of the world, and for several countries the region accounts for a high share of their agricultural exports. Processed agriculture accounts for more than half of total agricultural exports and is even more important in exports to the region.

Regional trade, whether measured in gross value terms or in value-added terms, is highly unbalanced in South Africa’s favour. This trade imbalance presents a political challenge to the process of integration because it provokes protectionist pressures (Black et al 2019). This could stall or even reverse moves towards successful regional integration.

Yet it also indicates that the South African market remains an opportunity for the development of export-oriented agricultural industries in other countries in the region. So what are the constraints to expansion of agricultural exports from the region to South Africa? While tariff barriers have largely been removed under the SADC free trade area, non-tariff barriers including sanitary and phytosanitary measures and technical barriers still constrain exports (Farole 2016), as do strict rules of origin (Brenton et al 2005).

All southern African countries have put industrial strategies in place to promote their respective manufacturing sectors. In most cases, agro-processing can be a key opportunity. But creating a stronger base of suppliers requires deliberate action.

There are several ways in which agriculture and agro-processing can be developed. More support for agriculture will be helpful. Another avenue is through incorporation into value chains, especially RVCs. Potential entry points for suppliers are supermarket chains and the associated large firms in the food industry. Many are South African owned. These firms comprise a large and growing market for agro-processed goods, and they have well-developed regional trade and production networks. However, accessing these supply chains is not easy. In addition to measures to mitigate these constraints, large firms, national and international agencies, and governments themselves have undertaken initiatives specifically aimed at supplier development. How can these be made more effective?

Supermarket chains (mainly South African based) have been expanding in the region for the past two decades and account for a growing share of consumer spending. What potential does this create for integrating local suppliers of agricultural products into their regional supply chains?

Shoprite Holdings is Africa’s largest retail chain and, compared with other major South African based chains, draws the highest share of its revenue from its operations in the rest of Africa (16.5% in 2015). In 2015, it had 250 stores in the rest of Africa with revenues of US$1.3 billion. While Shoprite recently reported a decline in quarterly sales in its ‘rest of Africa’ outlets and was considering reducing the number and size of stores or entering franchise arrangements, preserving their ‘African advantage’ remains one of its nine strategic goals (Crotty and Child 2019).

Pick n Pay also has large presence in the region. The number of stores outside of South Africa has grown rapidly (from 94 in 2012 to 148 in 2019), although its share of the total (including South Africa) declined from 10 to 8% over this period. Pick n Pay’s ‘rest of Africa’ strategy is seen as one of seven ‘growth acceleration’ pillars. Currently, however, problems in markets such as Zambia and Zimbabwe mean that its rest of Africa expansion has been ‘in hibernation’.

Much of the product in these stores is supplied from South Africa with relatively little returning in the opposite direction. This is graphically illustrated by the fact that trucks return empty to South Africa raising intra-African transport costs (Vilakazi 2018). Large retailers such as Pick n Pay and Shoprite source the bulk of the product sold in neighbouring supermarkets from within the country concerned but much of it is in turn supplied by large South African producers such as Tiger Brands and Pioneer Foods through their local distributors.

The supermarket chains and large food exporters have a strong interest in regional integration and in relaxing cross-border constraints. Weak infrastructure and delays at borders are extremely costly and hinder expansion (African Economic Outlook 2019). Transporting goods by truck from Cape Town to Johannesburg can take a day. The trip from Johannesburg to Lusaka in Zambia, a shorter distance, can take 5–8 days due mainly to border delays. Costs are increased by so-called ‘facilitation fees’.

The countries that host this South African retail expansion are increasingly concerned with the issue of domestic suppliers. With the support of local firms, neighbouring countries are starting to place pressure on the supermarket giants to expand domestic supply.3 Member states of SADC and SACU have imposed trade restrictions and local-content requirements on imports of certain food products from South Africa. For example, Zimbabwe has set a requirement that supermarkets purchase at least 20% of their products domestically. Botswana, Zambia, and Zimbabwe have placed bans on imports of cooking oil, maize meal, and poultry (Das Nair et al 2018). One of South Africa’s largest food companies, Pioneer Foods, which exports to 80 countries, attributed a recent decline in earnings as being partly caused by protectionism in African countries.4

All stakeholders have an interest in supplier development. More specifically, they have an interest in diversifying their supply base to protect the industry from potential shocks (Karingi et al. 2018; Phiri and Ziba 2019). Governments in the region also have an interest. This represents an opportunity to drive the development of agro-processing RVCs and thereby strengthen effective regional integration. What policies can make this happen?

The constraints on industrial development in the less developed countries of southern Africa are well known and include tariff and non-tariff barriers, weak infrastructure, demanding quality standards, and a weakly developed local supply base.

Average applied and MFN (Most Favoured Nation) rates are marginally higher in SADC than the rest of the world but because of higher volumes of lower protected goods, the weighted average MFN tariffs are lower. One reason is that a high proportion of food imports by SADC countries come from within SADC where there is a free trade agreement (FTA).

Lack of competition and high input costs present a further difficulty, including for larger firms in the region. An example is the Zambian sugar and confectionary industry, which has been unable to compete regionally due to two primary constraints: a lack of competition policy, and government imposed non-tariff barriers in the form of vitamin A fortification requirements on sugar (Das Nair et al 2017). Zambia imports almost no sugar because of this requirement, which protects the domestic industry. Zambia Sugar Plc’s market dominance and the lack of competition from imports means that Zambian sugar prices are higher than regional sugar prices. Zambia’s confectionary industry—processing raw sugar into sweets, biscuits, cakes, and so on—relies on Zambian sugar because of the restrictions on sugar imports. This industry is also relatively concentrated, partly because Zambia Sugar’s market dominance has meant that confectionary producers must have the power to negotiate lower sugar prices to survive (Das Nair et al 2017). Zambia exports some confectionary products—primarily to Malawi and Zimbabwe - but most producers are unable to compete with South African confectionary products in supermarkets.

Confectionary producers in Zambia argue that the only way for the industry to become more competitive is to lower trade barriers to sugar imports. The market dominance of Zambia Sugar has left confectionary producers vulnerable to price manipulation. In 2017, the Zambian Competition and Consumer Protection Commission fined Zambia Sugar for unfair pricing and price discrimination involving both household and ‘industrial sugar users’ (Funga 2017). However, competition in the sugar industry has yet to open up effectively.

South Africa is also adopting ad-hoc protectionist measures. As a result of declining sugar demand, partly driven by the introduction of a tax on sugar for health reasons, South Africa’s trade and industry department has reportedly placed pressure on large domestic firms to use South African sugar as much as possible. This is driving up local prices. Leaders of firms engaged in large scale regional trade are therefore sceptical of initiatives such as the AfCFTA because of their experience with border difficulties and non-tariff barriers.

Supplier development is fraught with challenges. The retail chains prefer to deal with large suppliers, and while they all have supplier development programmes aimed at small producers, the bulk of their business is with larger firms. For smaller firms, demanding standards and certification, competitive pricing, and large volume requirements present major obstacles. The availability of finance to upgrade capacity is a further constraint (African Economic Outlook 2019).

In their study of Zambia, Phiri and Ziba (2019) surveyed a range of firms, including those that did not supply supermarkets. The major constraint for these firms was finance but this related to the long credit times imposed by supermarkets. Another was the large volumes required by supermarket chains.

Packaging is also a challenge. Labeling, advisory, design, and testing services are limited, and the costs are high. These problems are more pronounced for small and medium-sized processors, which constitute the bulk of food manufacturers in Zambia.

Thus, firms attempting to access value chains by supplying supermarkets and large food companies face a daunting array of difficulties, many of which are outside of their control because they relate to governmental responsibilities. The outcome is underinvestment and limited upgrading. There are, however, a range of initiatives by large firms and non-profit and governmental agencies to not only provide the required productive assets but also access to markets.

Supermarket chains themselves have the capacity to upgrade suppliers. Indeed, they have all instituted supplier development programmes, partly in response to pressure from governments. Ironically, perhaps the most significant measure was the strong opposition by the South African government to Walmart’s bid to buy a controlling share in the South African chain, Massmart. The courts allowed the takeover, but a condition was the establishment of a R240 million Supplier Development Fund. This has met with some success and has been expanded beyond the initial required time frame. In this case governmental pressure led Massmart to expand its supplier development programme beyond what was required.

Such initiatives are also evident among South Africa’s neighbours. In Zambia, Shoprite has signed Memoranda of Understanding with the Zambia Development Agency (ZDA) and Private Enterprise Programme Zambia (PEPZ) to promote SMEs. Namibia also has a formal, albeit voluntary, retail charter (Das Nair et al 2018). This has been successful in developing local sourcing of fresh produce by Woolworths (Black et al 2019). The expansion and harmonization of such charters across the region may be a useful step in encouraging a more balanced approach to regional development, which encourages further regional integration.

Nando’s PERi farms project

Nando’s is a fast food restaurant chain, which by the end of 2018 had 937 fast food restaurants around the world (mainly in South Africa and the UK). Nando’s PERi farms project provides an interesting and successful example of domestic sourcing and social innovation. The company used to source chillies from the global marketplace, but 95% of Nando’s global requirements are now sourced from southern Africa, mainly from smallholders in Malawi, Mozambique, and Zimbabwe. International donors provided funding for the feasibility study, but the project does not require ongoing support and is seen as highly successful. It now involves 1,400 farmers in the three countries. They are assisted with extension services. Chilli farming is labour intensive and the crops are farmed on small plots. Nando’s has been able to establish prices and contracts directly with farmers avoiding low margins and volatile prices that can jeopardize the security of farmers. The impact on the incomes of smallholder farmers has been significant with notable improvements in indicators such as food security, education, and housing.

Various large firms have undertaken significant initiatives to upgrade suppliers. Apart from the initiative by Nando’s to source chillies from small farmers (see Box), the multinational Mount Meru Group is expanding out-grower schemes in Zambia with small-holder farmers. It is a major regional manufacturer of edible oil, soya oilcake, and other products produced from soya beans, cotton, and sunflower. It is also investing heavily in refinery, silo capacity, processing capabilities, and packaging units.

In most countries in the region, aid and non-profit agencies play a significant role. In Zambia, PEPZ is funded by the UK Department of International Development (DfID). Under the ‘Value Chain Strengthening Initiative’, PEPZ works on three broad themes: capital (co-investment and financial design), capacity (external technical and advisory assistance), and connections (fostering of market linkages).

In the soya bean value-chain, PEPZ brokered a deal with an agro-processor who initially worked with 400 farmers, but after PEPZ’s co-investment in the factory, the processor was able to buy soya beans from more than 1,000 farmers and increase tonnage. The processor’s capacity expanded by more than two-thirds. Farmers have also been trained, helping them increase yields and area cultivated. As a result, the quality of the soya beans produced has improved, positively impacting profitability.5

Similarly, Musika Zambia, a non-profit organization, is implementing a market development initiative in agricultural value chains, including legumes such as soya beans, which seeks to improve the ‘capacity of [the] food-processing industry to create commercially viable distribution channels for affordable nutritious foods into the rural market’.6 Musika’s development initiative helps to broaden the rural industrialisation base through strengthening agricultural commodity value-chains, value-addition activities, and the creation of non-farm employment.

These varied private and public initiatives have the common attribute of addressing coordination failures and missing markets across supply chains, and thereby facilitating entry by small and medium firms. Policy makers and aid donors need to develop strategies to encourage a rapid expansion of these ventures.

Regional value chains create potential for industrialisation in the region, but they are no silver bullet. Simply put, firms will invest where an economic case exists. Of course, the neighbouring countries would like to see industrial investment being ramped up. Arguably, South Africa has an interest in this too, insofar as a wider spread of the gains of integration is essential to keep the regional project on track. But does this trump South Africa’s interest in investment within its own borders? Almost certainly not. The same gloomy logic applies to supplier development by large supermarket chains or agro-processing firms. Although these firms have an interest in the development of the supply base across the region, investment decisions are going to be market based and much will have to change for this to happen on a significantly larger scale.

This raises a policy conundrum. How can industrialisation be driven forward in the region without resorting to protection? Some of the most important steps are generic. An improved regulatory and investment environment, the easing of border controls, better infrastructure and appropriate support services, and a clamp down on corruption will all lead to higher rates of investment and more rapid growth. Another fundamental measure would be greater support for agriculture to provide a supply-side push to the agro-processing sector.

South Africa needs to be more open to imports from the region and to play a more proactive role in driving a genuine ‘developmental regionalism’ agenda. This means infrastructure projects across borders and the easing of cross-border investment by South African firms. To be fair, there has been progress in that regard. Neighbouring countries in the region need to improve their operating environments and avoid protectionist measures. They could also, through ‘codes of conduct’, encourage multinational firms to localize and develop local suppliers.

The firms themselves need to take a far-sighted approach and see the longer-term benefits of a broader supply base. Commercial decision-making will enable some supplier development by large firms, although the tendency will be to underinvest without pressure and support from governments and non-profits. The key question is how supplier development can be most efficiently delivered. The examples of the programmes cited above may provide some clues. Certainly, international agencies and donors need to align support to incentivise investment in the supply base. Partnering with firms and governments, funding feasibility studies, and providing finance to small suppliers could all play a role.

Anthony Black is professor in the School of Economics at the University of Cape Town. He is a development economist whose main fields of expertise are industrial development, foreign investment and trade. Current research includes a major project on employment intensive growth in South Africa. He has been a leading advisor to government on South Africa’s programme to develop its automotive industry and has also acted as a consultant to the Government of Mozambique as well as to a number of international organisations such as UNIDO. International collaborations have included involvement in projects based at the London Business School, the World Institute of Development Economics Research (WIDER) in Helsinki and the International Motor Vehicle Program at MIT. He was Director of the School of Economics from 2003-2005.

Lawrence Edwards is Professor in the School of Economics, University of Cape Town, and a Research Associate of the South African Labour and Development Research Unit (SALDRU) and Policy Research on International Services and Manufacturing (PRISM) in the same institution. Lawrence is a graduate of the University of Cape Town where he completed his PhD, the London School of Economics and Political Science, and Rhodes University.

Lawrence’s research interests focus on international trade and labour, the determinants of trade flows and trade policy. He is the author (with Robert Lawrence) of Rising Tide: Is Growth in Emerging Economies Good for the United States and has published articles in World Development, Journal of International Development, Economics of Transition, Harvard Business Review and the South African Journal of Economics. His research has a strong policy oriented focus and has been conducted for institutions including the World Bank, the OECD, the African Development Bank, the South African National Treasury, the Department of Trade and Industry, the UK ESRC, IZA, CEPR/DFID and recently the Zambian and Swaziland governments.

Ruth Gorven was Educated at the University of Cape Town, completing her masters degree in the Economics of Development. She currently works for The Global Fund for the Fight Against HIV, Malaria, and Tuberculosis, supporting the development and implementation of various projects to enhance the organizations contribution to global health efforts. She has also previously worked as a consultant in the private sector, supporting a range of projects, including assisting on projects assessing the development of a range of African countries, as well as working with public sector players to distribute aid effectively.

Willard Mapulanga works as a policy analyst and researcher at the Zambia Institute for Policy Analysis and Research (ZIPAR) in Lusaka, Zambia. Before joining ZIPAR, he worked as a research assistant to Prof. Carlos Lopes, the 8th executive secretary (2012-2016) of the United Nations Economic Commission for Africa (UNECA), a current professor at the Nelson Mandela School of Public Governance, University of Cape Town (UCT) and High Representative of the Commission of the African Union. His main research interest is in regional economics, trade, political economy, climate change, and sustainable development. Willard is a Master of Development Economics and International Development graduate from the University of Cape Town (UCT) as a Mandela Rhodes scholar. He also holds a bachelor’s degree in Economics and Development Studies from the University of Zambia. Willard is a former president of the University of Zambia Business and Economics Association (UNZABECA).

This article is republished from Econ3X3 under a Creative Commons license. Read the original article here.

The views expressed in this piece are those of the author(s), and do not necessarily reflect the views of the Institute or the United Nations University, nor the programme/project donors.

For a full list of references, read the original article here.

1 According to World Development Indicator data, manufacturing value added as a share of Gross Domestic Product (GDP) in sub-Saharan Africa fell from 16 per cent in 1990 to 10 per cent in 2017. These average values hide important differences across countries. The manufacturing value-added share is as high as 19 per cent for Cameroon, Gabon, and Senegal, and 5 per cent or lower for Burkina Faso, Chad, Eritrea, and several others.

2 This data uses mirror data in 2010 and is therefore not as reliable as the other numbers in the table.

3 Kaplan, D., and M. Morris (2016). The expansion of South African based supermarkets into Africa: Likely future trajectory and the impact on local procurement and development. Cape Town: University of Cape Town, School of Economics, PRISM.

4 Njobeni, S. (2019). ‘Pioneer flags trade barriers’, Business Day. Published 19 November 2019.

5 Interview with a consultant at PEPZ, 22 August 2019

6 Interview with project officer at Musika Zambia, 20 August 2019